To the delight of skiers, recently Santa Fe has been inundated with a series of snowstorms, dumping about 4.5 feet of fresh powder on the local ski hill. As I headed down from the mountain after an early run, nervously navigating the descent on the treacherous snow-packed road, I was shocked at the number of cars heading up, packed with skiers hoping to carve a few turns in the best conditions in years. The line of cars formed another parking lot of sorts: uphill traffic that was stopped or barely moving extended over five miles down the mountain. As I inched by the first mile of hopeful skiers, it occurred to me that the overwhelming majority of these people would never ski a single run that day, but rather would be stuck in line amid dangerous and worsening blizzard conditions, as that reality slowly set it. I found this to be a fascinating case study in human behavior, in which many people had the same idea, which seemed like a great one: a fun day skiing fresh powder on the first weekend of the new year. The problem was that everyone had the same idea, and most of the crowd was heading up to implement it at the same time. As a result, for most the planned day of winter fun would end up as a frustrating exercise in wasted time, and a dangerous one as they attempt an exodus from the mountain in dangerous winter conditions on a crowded, snowy descent.

I was immediately struck by the parallels to investing, where the exact same human behavioral tendencies, and resultant benefits and costs, often apply.

As we begin 2024, it is worth recalling that one year ago, there was a strong consensus view held by Wall Street strategists: virtually all forecasts were negative on the global economy and investment outlook. The unanimity of strategist views was remarkable – virtually all called for a recession in 2024; the only difference was in the timing and severity of the recession forecasts. The reasons were manifest: annual CPI inflation in the US had recently hit 9.1%, and was higher elsewhere. After a late start, the Federal Reserve and other central banks had embarked on the most aggressive program of interest rate hikes in 40 years to combat rising prices, risking economic growth and recession as the price of taming inflation. Throughout the year, there were a series of events that startled investors, leading to a sense of malaise over markets for most of 2023, including multiple large bank failures and a fear that political debt ceiling battles might lead to a US bond default.

And yet a funny thing happened – stocks yet again climbed the proverbial “wall of worry”, and delivered exceptionally strong returns to investors who ignored the noise and incessant negative bleating of market commentators. In the US, large company stocks returned 26.3%. Foreign developed country stocks returned 18.8%, and emerging market stocks returned 10%. High yield bonds returned a robust 13.4%. Even high grade bonds, which had posted losses for most of the year, rallied hard in the last quarter and returned 5.5% for the year.

Rarely has there been a better reminder of the importance of ignoring the crowd, particularly when the consensus view has strayed too far to the positive, or to the negative as it did a year ago. In investing, as in skiing after a snowstorm, good ideas tend to be poor ideas for those who are late, and chase these ideas along with the crowd. As we so often advise, ignore the noise, stick with your plan, and view lower prices not as losses but rather as opportunities, and higher prices as potentially risky rather than confirmation of a benign environment.

As we begin 2024, we survey a very different landscape from both sentiment and asset valuation perspectives. After reviewing many 2024 Wall Street outlooks, it’s clear that most forecasters now have a somewhat benign middle-of-the road outlook for 2024, with bullish or bearish outliers not outlying by much. Few call for a 2024 recession. Predictably, market strategists again look backwards, and extrapolate 2023’s strong investment environment forward, although none I’ve read predict that 2023’s extraordinary stock market performance will be repeated – most call for single digit returns for both stocks and bonds this year. The common view now is that the economy may experience a “soft landing” – that the Fed may have artfully threaded the needle, subduing inflation without pushing the economy into recession. Perhaps.

Although another consensus therefore has emerged among market commentators, it is important to note that sometimes the consensus can be right, and the consensus is more likely to be right when expectations are for modest growth and investment returns, rather than excessively bullish, or bearish like last year.

Regarding major asset class valuations, stocks are about 25% more expensive than a year ago, given that prices have risen by that amount, while company earnings have remained basically flat. This leaves stocks about 30% more expensive than the long-term historical average. That does not mean that stocks should decline this year: earnings could materially increase, and in any case stock valuations are poor predictors of returns over the next 1-2 years. High grade bonds (represented by the Bloomberg US Aggregate Index) yield about 4.7% – exactly the same yield as a year ago, before big losses were followed by big gains.

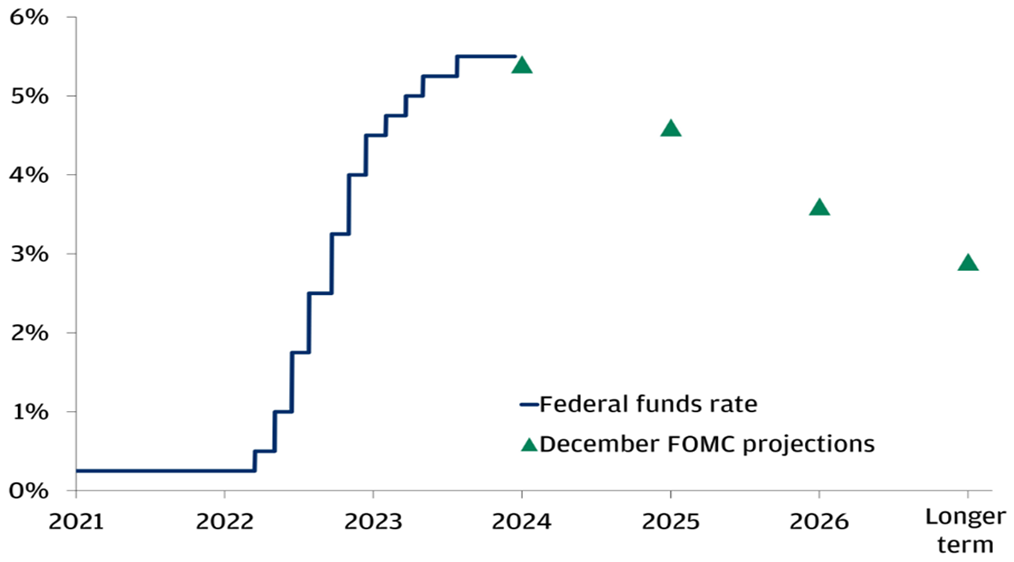

One major difference for investors now is that the Fed is expected to cut interest rates by 1.25-1.5% in 2024, whereas a year ago there were still several rate increases in the offing. See Graph 1 which shows the Fed’s forward policy rate projections.

Graph 1

Source: JPM, FRB, BBG

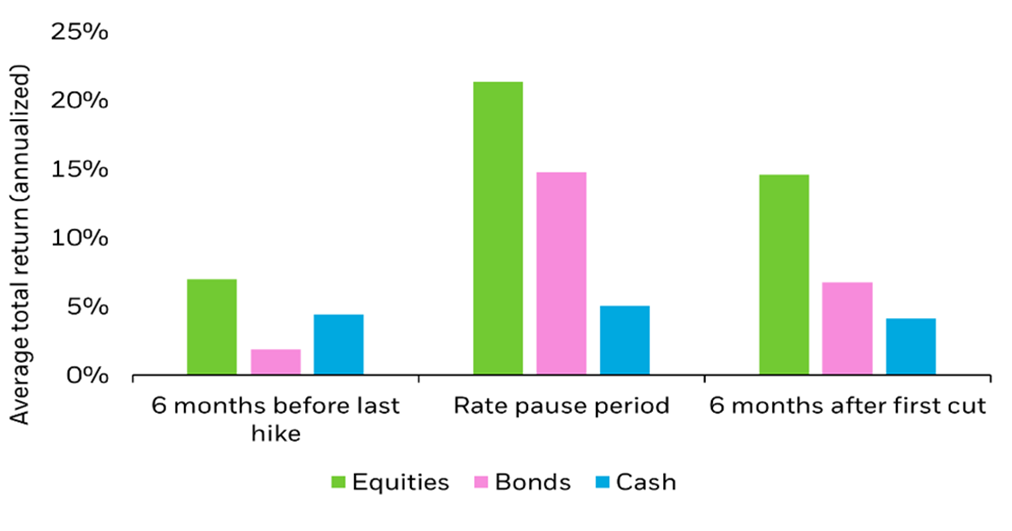

This augurs well for investors – the time from when the Fed nears the end of a tightening cycle (higher interest rates) and moves to an easing cycle (lower interest rates) has historically been an excellent time for investors in both stocks and bonds. Graph 2 shows returns of both asset classes as rate policy transitioned, and how both stocks and bonds tend to outperform cash during this period.

Graph 2

Source: BlackRock, BBG

So for now, given expectations of favorable monetary policy and a middle-of-the-road consensus (rather than an extreme bullish or bearish one) we believe that it is probably a reasonably favorable environment for both stocks and bonds as we start 2024. Of course, unexpected impactful events (both positive and negative) are likely to happen this year as always. Nevertheless, we currently believe that in this investment landscape the best approach is to keep risk near neutral long-term targets, and let market returns compound to our clients’ benefit

Thank you for your trust, and please contact a SFA team member with any questions, or to review the alignment of your portfolio with your personal circumstances.

The information contained within this letter is strictly for information purposes and should in no way be construed as investment advice or recommendations. Investment recommendations are made only to clients of Santa Fe Advisors, LLC on an individual basis. The views expressed in this document are those of Santa Fe Advisors as of the date of this letter. Our views are subject to change at any time based upon market or other conditions and Santa Fe Advisors has no responsibility to update such views. This material is being furnished on a confidential basis, is not intended for public use or distribution, and is not to be reproduced or distributed to others without the prior consent of Santa Fe Advisors.

To Top

To Top