It is the time of year when most people in our profession take stock of the events of the past year and start to think about what, if anything, those events might portend for the upcoming 12 months. In this case, 2025 was an unusually volatile year, with many unprecedented initiatives and announcements coming out of Washington that moved the markets in the short term, but had surprisingly little effect on the full year’s returns. The market remained broadly bullish despite the many geopolitical complications that occurred. For 2026, we remain cautious, or perhaps even apprehensive, about future returns given valuations and macro-level risks… but despite that, we remain fully invested, since it is rarely a good idea to bet against market sentiment.

Asset Class Returns in 2025

US markets turned in their third consecutive year of double-digit returns, with the S&P 500 up a strong 17.9% and the Russell 2500 Index of small and midcap stocks returning 11.9%. These returns were outstripped by the returns of non-US stocks, with developed markets and emerging markets having nearly identical returns, 31.2% and 31.4% respectively. The standout asset class was gold, returning a whopping 63.7% due to a great deal of geopolitical and economic uncertainty. Conversely, real estate produced a meager 2.8% return despite modest decreases in interest rates, usually good for real estate investments. The decrease in interest rates drove the Bloomberg Aggregate Bond Index to a 7.3% return, while the decline in the dollar pushed the Global Aggregate Bond Index to an 8.8% return in dollar terms, slightly better than the US High Yield Index return of 8.5%. Even short term bonds did well, with the Bloomberg 1-3 Year Government/Credit Index returning 5.3% as the Fed began to lower short term interest rates.

Chart 1

Source: Orion – Data as of December 31, 2025

Market Breadth

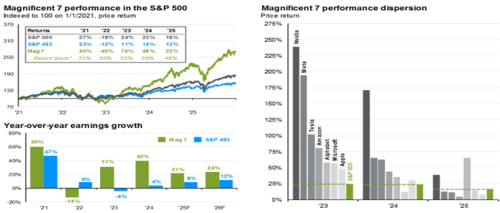

Large cap US growth stocks were the best performing sector in US securities markets, returning 19.2% vs. 15.9% for large cap US value stocks. This continues a rather tiresome trend that has persisted for most of the past ten years. The S&P 500 now exhibits a record level of concentration, with the ten largest stocks comprising an unprecedented 40% of the index. By comparison, that figure peaked in 2022 at just over 30%, and about 26% in 2000 during the dot-com bubble. The so-called Magnificent Seven (Mag 7) continue to dominate US equities, but less so than in recent years. As shown in Chart 2, the Mag 7 accounted for 46% of S&P 500 earnings in 2025, compared to 55% in 2024 and 63% in 2023. Perhaps more interestingly, only two of the seven Mag 7 stocks outperformed the S&P during the year…Nvidia (still riding the AI boom/bubble) and Alphabet (Google). More market breadth is likely to be good news over the long term for both investors and managers.

Chart 2

Source: JPM Guide to the Markets – Data as of December 31, 2025

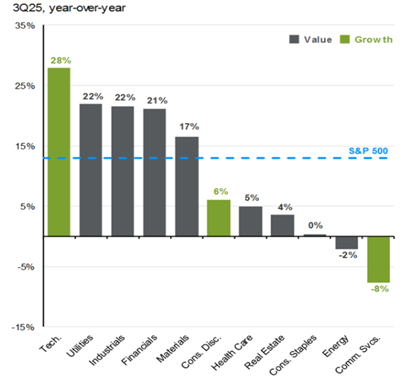

Notwithstanding the continuing strong price performance of large growth stocks, four of the five best-performing sectors of the S&P, measured by earnings growth, were traditional value sectors: utilities, industrials, financials, and materials, as shown in Chart 3. If this trend in earnings growth continues, then investment returns are likely to follow, as long term changes in enterprise value tend to be closely associated with changes in earnings.

Santa Fe Advisors maintains an overweight to US value stocks relative to growth, based on valuations and our views regarding relative valuations. We have maintained this position since early 2022. On balance, it has not had a positive effect on our returns, but we believe that the high valuations of large growth stocks cannot persist forever. Recent developments, particularly the underperformance of five of the seven Mag 7 stocks and superior earnings growth among value stocks, gives us hope that this positioning will produce positive results in the near future and provide protection from concentration risk in the S&P 500.

Chart 3

Source: JPM Guide to the Markets – Data as of December 31, 2025

Non-US Equities

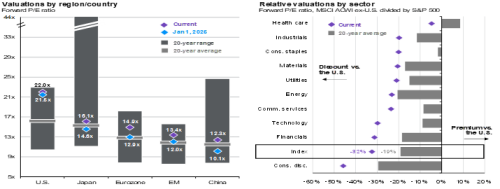

As noted earlier, non-US equities far outperformed those in the US for only the third time in the past 15 years. Despite this, valuations of non-US equities are relatively muted, with the MSCI ACWI Ex-US Index trading at a 32% discount relative to the US based on forward P/E ratios. Now, it is important to keep in mind that non-US equities almost ALWAYS sell at a discount to the US, the average being about 19%, so the fact that the ACWI is trading at a discount is nothing new (Chart 4). It’s the magnitude of the discount that is noteworthy. Having said that, this discount has persisted for many years, albeit at a lesser level, and there is no compelling reason to believe that it will narrow any time soon – unless relative earnings growth becomes stronger in overseas markets.

Chart 4

Source: JPM Guide to the Markets – Data as of December 31, 2025

Another major factor affecting non-US returns (both equities and fixed income) is currency movements (Chart 5). The US dollar tends to appreciate or depreciate against major foreign currencies in cycles that normally last 5-10 years. However, the last period of dollar appreciation ran for 14 years, from 2008 to 2022, and was concurrent with a very long period of US stocks outperforming their foreign counterparts. If we are, in fact, in a period of secular dollar weakness, as many forecasters expect, then that could break the very long run of US equity outperformance.

Chart 5

Source: JPM Guide to the Markets – Data as of December 31, 2025

Fixed Income

US fixed income returns improved markedly during the year, as was noted earlier. Real yields on the 10-year Treasury are still a bit below historical averages, at 1.56% compared to a long term average of 1.92%, but they increased dramatically in the fourth quarter (Chart 6). The real yield is the stated (nominal) yield minus inflation. The yield curve moved significantly during the year and is now normally shaped, other than slightly elevated levels at the very short end of the curve (and therefore a very modest inversion out to three years). The dramatically inverted curve that we saw in 2023 is a thing of the past and despite assertions by some that an inverted yield curve was a sure sign of a recession, it never happened. Or perhaps better to say that it hasn’t happened yet, and there’s no sign of one in the offing.

Chart 6

Source: JPM Guide to the Markets – Data as of December 31, 2025

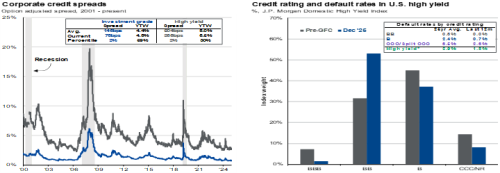

The spreads on investment grade and high yield bonds are both about half of their long-term historical averages. The investment grade spreads are currently 78 basis points (0.78%) compared to an average of 140 (1.40%), and high yield spreads are 266 basis points compared to an average of 504 (Chart 7). The big difference here is that investment grade YIELDS are actually slightly above average…4.8% vs. 4.4%…whereas high yield yields are well below average…6.5% vs an average of 8.0%. Defaults remain quite low across the board, which is no doubt why the high yield spreads in particular have been pushed to such modest levels.

Chart 7

Source: JPM Guide to the Markets – Data as of December 31, 2025

Effects on SFA Portfolios

The SFA Investment Committee (myself, Kristina, Lincoln, and George Strickland) recently met for several hours to discuss these and other factors and begin the discussion about whether we want to make any changes to our portfolio. As yet, we have not come to any conclusions and are unlikely to make major changes. There are, however, a few initiatives and “tweaks” that we are considering:

- Reduce or eliminate our allocation to real estate equity, which has produced disappointing returns, and reallocate those funds to US equities. In most cases, this would only involve the movement of a few percent of the portfolio.

- We have affirmed our position in non-US equities, which comprises over 40% of our total equity holdings in most of our portfolios. This is much higher than most managers maintain and served us well over the past year. If the current trends, particularly with the dollar, continue, this is likely to add value over the next few years.

- Reduce or eliminate our allocation to high yield fixed income, for the reasons outlined above. Spreads in both high yield and investment grade bonds are below average, but yields on investment grade bonds are, relative to the historical average, superior.

We expect a great deal of volatility in 2026, given geopolitical factors and the inability to have a good sense of what policies or rhetoric might be issued from Washington. Nonetheless, it is entirely possible that equities will continue their strong run. We do not invest based on our ability to guess what is going to happen in the markets over the next few months, an ability that we (and everyone else) unfortunately do not possess. Instead, we focus on applying an appropriate level of risk to portfolios based on the time horizon and level of growth needed.

The information contained within this letter is strictly for information purposes and should in no way be construed as investment advice or recommendations. Investment recommendations are made only to clients of Santa Fe Advisors, LLC on an individual basis. The views expressed in this document are those of Santa Fe Advisors as of the date of this letter. Our views are subject to change at any time based upon market or other conditions and Santa Fe Advisors has no responsibility to update such views. This material is being furnished on a confidential basis, is not intended for public use or distribution, and is not to be reproduced or distributed to others without the prior consent of Santa Fe Advisors.

To Top

To Top